Foreign Trade Zone vs Bonded Warehouse: A Decision Framework for Duty Deferral, Cost Savings, and Smarter Import Strategy

If you’re importing goods into the United States and paying customs duties the moment each shipment clears the port, you’re handing over working capital that could be sitting in your bank account for months – or even years. Foreign Trade Zones (FTZs) and bonded warehouses both offer legitimate, government-authorized ways to defer, reduce, or even eliminate those duty payments. But they work differently, cost differently, and fit different types of businesses.

This guide goes beyond surface-level definitions. We’ll walk you through how duty deferral actually works in each structure, compare the real costs and compliance requirements, and give you a practical decision framework – including qualification checklists and break-even logic – so you can figure out which option fits your import volume, product mix, and growth trajectory. And because choosing a structure is only half the challenge, we’ll also cover what it takes to make either one work operationally.

TL;DR (Key Takeaways)

- Both FTZs and bonded warehouses let you defer customs duties until goods enter U.S. commerce, but FTZs offer additional benefits like the inverted tariff advantage, weekly entry consolidation, and unlimited storage time.

- Bonded warehouses are simpler to access and better suited for importers who primarily need duty deferral on stored goods without manufacturing, while FTZs reward manufacturers and high-volume importers with greater cost savings potential.

- The five-year storage limit in bonded warehouses versus unlimited FTZ storage matters significantly for slow-moving inventory or goods held pending tariff changes.

- With Section 301 tariffs, shifting trade policy, and ongoing tariff volatility, duty deferral strategies have moved from ‘nice to have’ to essential for many importers.

- Neither structure eliminates the need for customs expertise – both require accurate classification, compliant recordkeeping, and coordinated freight logistics to deliver real savings. A trusted freight and customs partner is not optional; it is the mechanism through which these strategies actually work.

Why Duty Deferral Matters More Than Most Importers Realize

Most importers treat customs duties as a fixed cost of doing business – a line item that gets paid at entry and forgotten. But duties aren’t just a cost. They’re a cash flow decision. Every dollar you pay in duties at the port is a dollar that’s not available for inventory, marketing, payroll, or growth. And when you’re importing goods that might sit in a warehouse for weeks or months before they sell, you’re essentially financing the government’s revenue collection on goods that haven’t generated a dime of income yet.

Duty deferral is the practice of postponing when you pay customs duties – sometimes until goods actually enter U.S. commerce, sometimes indefinitely if they’re re-exported. It’s distinct from duty reduction (paying a lower rate) and duty elimination (not paying at all), though FTZs can offer all three under the right circumstances.

The cash flow impact most importers overlook

Consider a straightforward scenario. You import $500,000 worth of consumer electronics from China every month. With a combined duty rate of 25% (base tariff plus Section 301 duties), you’re paying $125,000 in duties each month at entry. If your average inventory cycle is 90 days – meaning it takes three months from the time goods arrive until they sell – you’ve got roughly $375,000 in duty payments tied up in unsold inventory at any given time.

Now, imagine deferring those payments until goods actually leave for domestic sale. That $375,000 stays in your operating account, available for purchasing more inventory, covering operating expenses, or simply earning interest. Over the course of a year, the opportunity cost of that trapped capital – even at a modest 5% cost of capital – works out to nearly $19,000 in lost value. Scale that up with higher import volumes or higher duty rates, and the numbers become impossible to ignore.

This impact hits hardest for businesses importing from high-tariff origins. Section 301 tariffs on Chinese goods currently range from 7.5% to 100%, depending on the product category, and the effective tariff rate on many Chinese goods shipped to the U.S. remains close to 30% when all applicable duties are stacked together. For importers dealing with those rates, every month of deferred payment is meaningful.

Working with a freight and customs partner who monitors tariff developments in real time – and who can flag when shifting rates change the calculus on your deferral strategy – is what separates a plan that looks good on paper from one that actually delivers savings in practice.

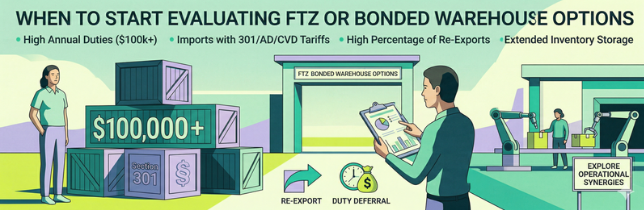

When to start evaluating FTZ or bonded warehouse options

Not every importer needs a duty deferral strategy. But if any of the following describe your situation, it’s worth exploring:

- Your annual duty payments exceed $100,000 and represent a significant share of your cost of goods sold.

- You import goods subject to Section 301 tariffs, antidumping duties, or countervailing duties.

- A meaningful percentage of your imports are re-exported rather than sold domestically.

- Your inventory sits in storage for extended periods before entering the domestic market – common for seasonal products, strategic reserves, or goods awaiting market conditions.

- You already use third-party warehousing or logistics partners, which means the operational infrastructure for FTZ or bonded warehouse participation may already be partially in place.

- Your duty rates are above 10%, where even modest deferral periods generate noticeable cash flow benefits.

If you checked multiple boxes, keep reading. The next sections will help you understand exactly what each structure offers and which one aligns with your business.

What Is a Foreign Trade Zone (FTZ)?

A Foreign Trade Zone is a designated area within the United States that is legally considered outside of U.S. customs territory for duty purposes. That distinction is the key to everything an FTZ offers. Goods can be brought into an FTZ – stored, assembled, manufactured, tested, displayed, and even destroyed – without triggering customs duty obligations. Duties are only assessed when goods formally enter U.S. commerce, and they’re eliminated entirely if goods are re-exported.

FTZs are authorized under the Foreign-Trade Zones Act of 1934 and regulated by two entities: the FTZ Board (under the U.S. Department of Commerce) and U.S. Customs and Border Protection (CBP). The legal framework is found in 15 CFR Part 400 (FTZ Board regulations) and 19 CFR Part 146 (CBP regulations).

There are two main types. General-purpose zones are multi-user facilities, often located in industrial parks or near ports, where multiple companies can operate under FTZ procedures. Subzones (or ‘usage-driven sites’ under the newer Alternative Site Framework) are designated for a specific company’s operations, typically at their own manufacturing or distribution facility. According to the National Association of Foreign-Trade Zones, there were 197 active FTZ programs across the United States as of the most recent annual report to Congress, employing approximately 550,000 people across roughly 1,300 active operations.

How duty deferral works inside an FTZ

The core mechanism is straightforward: goods admitted to an FTZ are not subject to duties until they are transferred out of the zone and into U.S. commerce. But the specifics create several layers of financial advantage.

Weekly entry consolidation. Instead of filing a separate customs entry for each shipment, FTZ operators can consolidate all withdrawals during a seven-day period into a single weekly entry. This directly reduces the number of Merchandise Processing Fees (MPF) you pay. The current MPF rate is 0.3464% of the goods’ value, with a minimum of $33.58 and a maximum of $651.50 per entry for fiscal year 2026. If you’re filing dozens of entries per month, consolidating into weekly entries can save thousands of dollars annually in MPF alone.

Inverted tariff benefit. This is one of the most powerful FTZ advantages for manufacturers. If imported components carry a higher duty rate than the finished product they’re assembled into, FTZ users can elect to pay the lower finished-product rate. For example, if you import electronic components at a 5% duty rate but the assembled device carries a 2% rate, you pay the 2% rate on goods withdrawn for domestic consumption. This benefit depends on electing non-privileged foreign (NPF) status for the imported components. It’s worth noting that recent trade remedy tariffs (including Section 301 and Section 232 duties) require goods to be admitted in privileged foreign (PF) status, which locks in the duty rate at the time of admission and limits the inverted tariff benefit for those specific goods.

Duty elimination on re-exports, waste, and scrap. Goods that are re-exported from an FTZ never incur U.S. customs duties. Likewise, scrap and waste generated during manufacturing processes within the zone can be destroyed or disposed of without duty payment – a meaningful benefit for operations with significant material loss rates.

No time limit on storage. Unlike bonded warehouses, FTZs impose no statutory time limit on how long goods can remain in the zone. As long as the zone is active and compliant, merchandise can stay indefinitely.

FTZ operational requirements and compliance

Operating within an FTZ carries real compliance overhead. The zone must be activated by CBP before any merchandise can be admitted, and that activation process involves demonstrating adequate physical security, inventory control systems, and recordkeeping procedures.

FTZ operators must maintain detailed inventory tracking that follows merchandise from admission through any manipulation, manufacturing, or processing, all the way to withdrawal or export. Annual reconciliation is required, and both CBP and the FTZ Board conduct audits. The FTZ Board’s regulations and CBP’s oversight requirements are extensive, covering everything from physical access controls to detailed reporting on zone activity.

For production activity (manufacturing, assembly, or processing that results in a change of tariff classification), the FTZ Board must grant specific authorization. This adds another layer of application and review before operations can begin.

Most importers don’t operate their own FTZ. Instead, they work through an FTZ operator or grantee – a third-party entity that manages the zone infrastructure, compliance systems, and CBP interface. This is the most practical path for businesses that want FTZ benefits without building the compliance apparatus from scratch. The right logistics partner doesn’t just manage the freight leg – they coordinate directly with FTZ operators and your customs broker to ensure that admission, manipulation, and withdrawal procedures are handled correctly from day one.

Who benefits most from an FTZ

FTZs deliver the highest return for specific business profiles:

- Manufacturers and assemblers who process imported components into finished goods, especially where inverted tariff opportunities exist.

- High-volume importers who file enough entries to generate meaningful MPF savings through weekly entry consolidation.

- Companies with significant re-export activity, where duty elimination on re-exported goods directly impacts margins.

- Businesses with long inventory holding periods that benefit from indefinite deferral without time pressure.

- Importers navigating tariff uncertainty who want the flexibility to hold goods and defer classification decisions while trade policy evolves.

What Is a Bonded Warehouse?

A bonded warehouse is a CBP-licensed facility where imported goods can be stored for up to five years without payment of customs duties. Authority for bonded warehouses comes from 19 U.S.C. § 1555, and the operational regulations are found in 19 CFR Part 19.

The concept is simple: when goods enter a bonded warehouse, the warehouse proprietor assumes liability for the merchandise under a customs bond. Duties are deferred until goods are withdrawn for consumption – meaning they formally enter the U.S. domestic market. If goods are exported, destroyed under CBP supervision, or transferred to another bonded facility, duties are never paid.

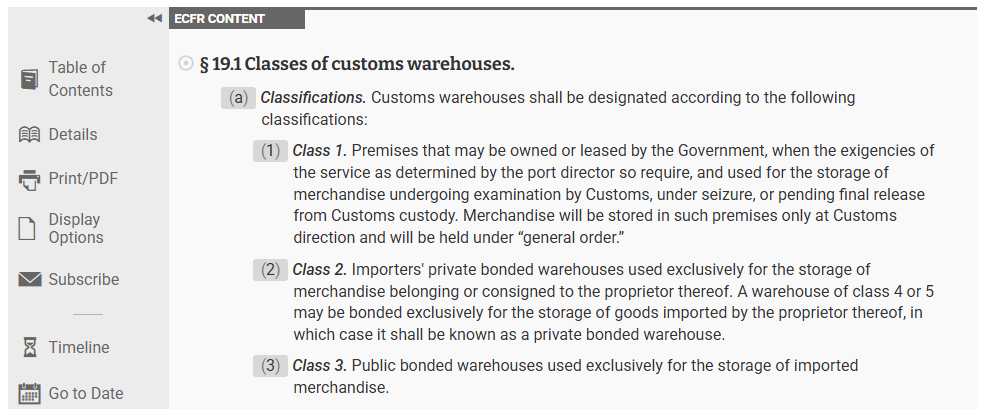

There are eleven classes of bonded warehouses defined under 19 CFR 19.1, each serving different functions. The most relevant for general importers are Class 2 (private bonded warehouses for a single proprietor’s goods), Class 3 (public bonded warehouses for storage of imported merchandise), and Class 8 (warehouses for cleaning, sorting, repacking, or otherwise changing the condition of imported goods – but not manufacturing).

How duty deferral works in a bonded warehouse

Bonded warehouse duty deferral is more straightforward than the FTZ mechanism, but also more limited in scope.

Duties are deferred for up to five years from the date of import. During that period, goods must remain in the bonded facility under CBP custody. When goods are withdrawn for consumption (entering the domestic market), a customs entry must be filed and duties paid at that point. Each withdrawal requires its own entry – there is no weekly entry consolidation like in an FTZ.

Unlike FTZs, bonded warehouses do not offer the inverted tariff benefit. You pay duties based on the goods’ classification and the rate in effect, without the ability to elect a lower finished-product rate. However, there’s one notable nuance: because bonded warehouse duties are assessed at the time of withdrawal rather than admission, the rate applied is the rate in effect at withdrawal. If tariffs decrease between the time goods are warehoused and the time they’re withdrawn, you pay the lower rate. This is the opposite of FTZ privileged foreign status, where the rate is locked at the time of admission.

Goods that are re-exported from a bonded warehouse are not subject to duty payment, which parallels the FTZ treatment. Goods can also be transferred to another bonded facility without triggering duties.

Bonded warehouse operational requirements and compliance

Bonded warehouses operate under strict but comparatively straightforward CBP compliance requirements. The proprietor must obtain a customs bond (either a continuous bond or single-entry bond), maintain detailed inventory control and recordkeeping, and provide physical security and controlled access to the bonded area.

The critical constraint is the five-year time limit. Under 19 CFR 144.5, merchandise must not remain in a bonded warehouse beyond five years from the date of importation (unless the Center Director grants an extension for good cause). After five years, goods must be exported, entered for consumption, or face disposition by CBP.

Bonded warehouses also face restrictions on what can be done with goods. Class 8 warehouses allow cleaning, sorting, repacking, and similar conditioning activities, but manufacturing is not permitted. This is a fundamental limitation that shapes which businesses benefit from bonded warehousing versus FTZ participation.

CBP conducts periodic audits, and proprietors must take at least an annual physical inventory of all merchandise. The recordkeeping requirements are real, but they’re generally less complex than FTZ reporting obligations since there’s no FTZ Board oversight layer and no production-activity authorization process. A logistics provider with customs brokerage capabilities embedded in the same workflow – rather than handled as a separate engagement – can significantly reduce the administrative burden of meeting these requirements consistently.

Who benefits most from a bonded warehouse

Bonded warehousing is the better fit for several common import scenarios:

- Importers who primarily re-export, where duty elimination on re-exported goods is the main value driver.

- Businesses with unpredictable demand that need to hold inventory before committing to domestic entry and duty payment.

- Companies importing goods subject to quota restrictions, where bonded storage provides time flexibility until quotas open.

- Traders and distributors who consolidate and redistribute imported goods across different markets or customers.

- Importers who need time to arrange financing before paying duties, using the deferral period to manage cash flow around buyer payments.

- Smaller-scale importers whose volume doesn’t justify the higher setup costs and compliance overhead of FTZ participation.

- Importers anticipating tariff reductions who may benefit from the bonded warehouse rule that applies the duty rate in effect at withdrawal rather than at admission.

FTZ vs Bonded Warehouse: Key Differences That Affect Your Decision

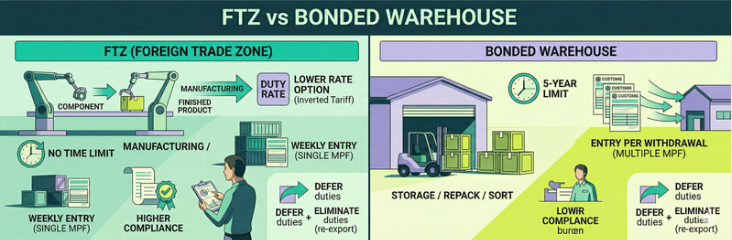

Both structures defer duties. Both eliminate duties on re-exports. But the similarities end there. The differences in how each structure works – what activities are allowed, how entries are processed, what compliance demands they impose, and what they cost – are what should drive your decision.

Duty mechanics: deferral, reduction, and elimination

Both FTZs and bonded warehouses defer duties until goods enter domestic commerce, and both eliminate duties on goods that are re-exported. The critical difference is that FTZs offer additional avenues for duty reduction that bonded warehouses simply don’t provide.

The inverted tariff benefit is exclusive to FTZs. If you manufacture or assemble products using imported inputs, and the finished product has a lower duty rate than the components, the FTZ lets you pay the lower rate. Bonded warehouses offer no rate optimization – you pay whatever rate applies to the goods as classified.

Weekly entry consolidation in FTZs reduces total MPF payments. In a bonded warehouse, each withdrawal is a separate entry with its own MPF charge. For businesses making frequent withdrawals, this difference adds up quickly.

FTZs also allow duty elimination on waste, scrap, and goods destroyed within the zone during manufacturing. Bonded warehouses offer limited destruction options but no comparable benefit tied to manufacturing processes (since manufacturing isn’t permitted).

Allowable activities: storage vs. manufacturing and processing

This is the single most important operational distinction. Bonded warehouses are for storage and limited manipulation – cleaning, sorting, repacking, and similar conditioning. No manufacturing, assembly, or substantial transformation is allowed.

FTZs permit the full range of activities: storage, assembly, manufacturing, processing, testing, exhibition, and display. A company can import raw materials or components, assemble them into finished products, and then either export them duty-free or enter them into U.S. commerce at the finished-product duty rate (subject to the status and tariff considerations discussed earlier).

This distinction matters enormously for businesses that add value to imported inputs. If you import electronic components and assemble finished devices, or if you import bulk ingredients and blend them into consumer products, only an FTZ supports that workflow within the duty-deferral framework.

Storage time limits

Bonded warehouses impose a strict five-year limit from the date of importation. After five years, goods must be exported, entered for consumption with duty payment, or they face disposition (potential sale) by CBP.

FTZs have no statutory time limit. Goods can remain in a zone indefinitely, as long as the zone is active and the operator maintains compliance. This matters for slow-moving inventory, strategic reserves, goods held pending market conditions, or merchandise held while tariff policy evolves.

Entry process and merchandise processing fees

In a bonded warehouse, every withdrawal for consumption requires a separate customs entry filing. Each entry incurs the MPF – currently 0.3464% of value, with a minimum of $33.58 and a maximum of $651.50 per entry.

In an FTZ, operators can consolidate all withdrawals during a seven-day zone week into a single entry. This means one MPF charge covers an entire week of shipments, regardless of how many individual withdrawals occurred. For an importer making 20 withdrawals per week from a bonded warehouse, that’s 20 MPF charges versus one in an FTZ. At the maximum fee of $651.50 per entry, the difference is over $12,000 per week – more than $600,000 annually.

Even at lower volumes, the savings are meaningful. An importer filing 50 entries per month at the minimum MPF of $33.58 each would pay roughly $20,000 annually. Consolidating to weekly entries in an FTZ drops that to approximately $1,750 per year.

Compliance burden and operational complexity

FTZs carry a heavier compliance load. Operators must satisfy both the FTZ Board (Commerce Department) and CBP. Recordkeeping must track every item from admission through manipulation, manufacturing, and withdrawal. Annual reconciliation, production-activity authorization, and physical security requirements all add to the operational overhead. Most businesses need either dedicated in-house compliance staff or a specialized FTZ operator to manage the burden.

Bonded warehouses are regulated by CBP alone. The compliance requirements – bonding, inventory control, annual physical inventory, and access controls – are strict but more contained in scope. For businesses with competent customs brokerage support, bonded warehouse compliance is generally more accessible.

That said, neither structure is set-and-forget. Both require ongoing attention to classification accuracy, entry procedures, and regulatory changes. Errors in either environment can trigger penalties, duty assessments, and potential loss of authorization.

Cost structure: setup, ongoing, and hidden costs

FTZ costs include activation fees, FTZ operator or grantee fees, investment in compliant inventory control systems, ongoing reporting and reconciliation costs, and potentially subzone application fees. For businesses using a third-party FTZ operator, monthly or annual operator fees are typical. Compliance system implementation can represent a meaningful upfront investment.

Bonded warehouse costs include customs bond premiums (typically a percentage of the maximum duty and tax liability), warehouse storage fees (which may be higher than non-bonded storage due to the security and compliance requirements), per-entry customs brokerage fees for each withdrawal, and potential penalties for compliance failures.

The right comparison isn’t just ‘which costs less?’ – it’s ‘which generates net savings after accounting for all costs?’ That’s the break-even question we address in the decision framework below.

Decision Framework: Which Option Fits Your Business?

Choosing between an FTZ and a bonded warehouse isn’t about which structure is ‘better’ in the abstract. It’s about which one matches your specific import profile, operational capabilities, and financial goals. The following checklists and break-even framework will help you evaluate.

Qualification checklist: is an FTZ right for you?

An FTZ is likely the stronger fit if most of the following apply to your business:

- You manufacture, assemble, or process imported components in the United States – not just store them.

- Your finished products carry a lower duty rate than the imported inputs (inverted tariff opportunity), and those products are not subject to mandatory privileged foreign status requirements.

- You import at high volume and frequency, generating enough entries that weekly entry consolidation produces meaningful MPF savings.

- You re-export a significant share of imported goods, benefiting from complete duty elimination on those exports.

- You need the flexibility to hold inventory indefinitely without a storage deadline.

- You’re prepared to invest in compliance infrastructure – either by building in-house capability or partnering with an experienced FTZ operator.

- Your annual duty exposure is substantial enough (typically six figures or higher) to justify the setup and ongoing costs of FTZ operations.

Qualification checklist: is a bonded warehouse right for you?

A bonded warehouse is likely the better fit if most of these apply:

- Your primary need is duty deferral on stored goods, not manufacturing or assembly.

- You re-export a significant portion of your imports and want duty elimination on those goods without the overhead of FTZ compliance.

- You need time flexibility before committing goods to domestic entry – for financing, market timing, or demand planning – but your inventory cycles are well within the five-year window.

- Your import volume and entry frequency don’t justify the higher activation and operating costs of an FTZ.

- You want a simpler compliance model that doesn’t require FTZ Board authorization or production-activity approvals.

- You’re anticipating potential tariff reductions and want the ability to pay the duty rate in effect at the time of withdrawal rather than at the time of admission.

Break-even logic: when the numbers make the decision

At its core, the decision comes down to whether the duty savings and cash flow benefits from either structure exceed the costs of operating within it. Here’s a simplified framework for evaluating that:

Key variables to gather:

- Annual duty exposure – Total customs duties paid per year under current procedures.

- Duty rate(s) – The applicable rate(s) on your primary import categories.

- Re-export percentage – What share of imported goods are re-exported rather than sold domestically.

- Inventory holding period – Average time goods sit before entering domestic commerce.

- Entry frequency – Number of customs entries filed per year.

- MPF exposure – Total annual MPF payments under current entry filing patterns.

- Cost of capital – Your company’s borrowing rate or opportunity cost of deployed capital.

Simplified break-even formula:

If (annual duty savings from deferral × cost of capital) + (MPF reduction from weekly entry) + (duty elimination on re-exports) + (inverted tariff savings, if applicable) exceeds (annual cost of FTZ operation or bonded warehouse fees + compliance overhead), the structure pays for itself.

Example scenario – FTZ evaluation: An importer pays $1.2 million in annual duties, files 200 entries per year, and re-exports 15% of goods. At a 6% cost of capital with a 90-day average deferral, the cash flow benefit alone is roughly $18,000. MPF consolidation from 200 entries to 52 weekly entries saves approximately $96,000 in MPF fees (at the maximum $651.50 per entry). Duty elimination on re-exports saves $180,000. Total potential savings: approximately $294,000 per year. If FTZ operating costs (operator fees, compliance systems, reporting) are $80,000–$120,000 annually, the FTZ clearly pays for itself.

Example scenario – Bonded warehouse evaluation: A smaller importer pays $200,000 in annual duties, files 40 entries per year, and re-exports 30% of goods. The cash flow benefit from deferral is more modest (perhaps $3,000–$5,000 annually), but duty elimination on re-exports saves $60,000. If bonded warehouse fees and bond costs total $15,000–$25,000 per year, the bonded warehouse delivers a strong ROI – and the compliance burden is manageable.

The specifics will vary based on your actual duty rates, import patterns, and operational costs. A customs and logistics partner with access to your real import data can run this analysis with precision. At Unicargo, this is typically one of the first exercises our trade compliance team conducts when onboarding a new client – mapping actual entry data against both structures to surface where the savings opportunity genuinely lives before any commitment is made.

Can you use both? Hybrid and transition scenarios

Yes. Businesses can use both an FTZ and a bonded warehouse simultaneously, often for different product lines or import flows. A common hybrid approach uses bonded warehousing for goods that are primarily stored and redistributed, while routing manufacturing inputs through an FTZ for inverted tariff and production-related benefits.

Another common path is transitioning from a bonded warehouse to an FTZ as import volume grows. Many importers start with bonded warehousing as a lower-barrier entry point for duty deferral, then evaluate FTZ activation once their duty exposure, entry volume, or manufacturing activities reach a threshold where FTZ-specific benefits justify the investment.

Managing hybrid structures requires coordination across customs brokerage, freight logistics, and warehouse operations – exactly the kind of orchestration where an integrated logistics partner adds the most value. Having freight forwarding, customs brokerage, and warehousing under a coordinated operating model means that the documentation, in-bond transfers, and compliance requirements for parallel structures don’t fall through the cracks between disconnected providers.

What Most FTZ and Bonded Warehouse Guides Don’t Tell You

You still need customs expertise to make either option work

Neither an FTZ nor a bonded warehouse replaces the need for skilled customs brokerage. In fact, both structures increase the stakes around classification accuracy, entry procedures, and compliance management.

In an FTZ, correct tariff classification is critical, especially when evaluating inverted tariff opportunities. If you misclassify an imported component or the finished product, you may claim a duty reduction you’re not entitled to, triggering penalties and potential loss of FTZ privileges. FTZ reporting and annual reconciliation require specialized knowledge that most general customs brokers don’t routinely handle.

In a bonded warehouse, every withdrawal requires a compliant customs entry. Errors in classification, valuation, or entry processing can negate your duty savings or create liability. And the five-year time limit means you need systematic tracking to ensure goods are entered or exported before the deadline – missing it means CBP can take action on your merchandise.

Tariff changes add another layer of complexity. Section 301 tariffs, antidumping and countervailing duties, and shifting trade policy all affect duty rates and classification requirements. What was a good duty deferral strategy six months ago may need adjustment based on new proclamations or regulatory changes. For importers already grappling with how long customs clearance takes under normal conditions, adding FTZ or bonded warehouse procedures without proper expertise can compound delays rather than reduce costs.

Unicargo’s embedded customs brokerage team works within the same operational workflow as our freight and warehousing teams. Classification decisions, entry filings, and compliance monitoring aren’t handed off to a separate provider — they’re part of the same coordinated service, which means errors get caught before they become penalties.

Getting goods into the zone or warehouse: the freight and logistics layer

Duty deferral only delivers value if goods arrive at the right facility, with the right documentation, in compliance with all applicable procedures. That’s a freight forwarding and logistics challenge.

Moving goods into an FTZ or bonded warehouse requires coordination of international freight (ocean, air, or land), customs clearance, and in-bond transportation procedures. ISF (Importer Security Filing) must be filed in advance. Documentation – including commercial invoices and packing lists – must be complete and accurate. And the handoff between freight forwarder, customs broker, and warehouse operator must be seamless – delays or documentation errors at any step can create compliance issues or negate the cash flow benefits of deferral.

For importers shipping from China or other major origin countries, the freight leg involves coordinating across time zones, carriers, and port operations. Goods need to arrive at a port near the FTZ or bonded warehouse and be transferred under proper in-bond procedures. Unicargo maintains a team on the ground in China whose sole focus is managing origin-side coordination – booking freight, preparing documentation, and aligning the entire chain so that by the time goods depart the origin port, every downstream step in the U.S. is already in motion. Businesses without an established U.S. presence may also need Importer of Record (IOR) services to serve as the legal entity responsible for compliance and duty payments – a capability Unicargo supports directly.

When freight, customs, and warehousing are managed under one coordinated operating model rather than across disconnected vendors, the friction points that typically generate delays and documentation errors largely disappear. The difference is material – both in compliance outcomes and in whether the financial case for duty deferral actually holds up month after month.

Tariff volatility and the need for ongoing compliance monitoring

The trade policy landscape has shifted dramatically in recent years, and the pace of change shows no sign of slowing. In February 2026, the U.S. Supreme Court struck down the administration’s use of the International Emergency Economic Powers Act (IEEPA) as the legal basis for a broad set of tariffs, ruling that the executive branch had exceeded its authority in applying that statute to import duties at the scale it had. The decision was a significant legal development, effectively invalidating a category of tariff actions and triggering a rapid policy pivot. The administration responded by shifting to Section 122 of the Trade Act of 1974 – a different statutory vehicle that permits temporary tariffs for balance-of-payments purposes – while also initiating new Section 301 investigations targeting 16 additional trading partners.

Important note: Trade policy moves faster than any static publication can track. The developments described above reflect the state of affairs as of early 2026, but regulations, tariff rates, HS code classifications, and applicable statutes can change with little notice. Before making any structural decision about FTZs, bonded warehouses, or your overall duty deferral strategy, verify current requirements with your freight forwarder, licensed customs broker, and trade counsel. What was accurate when this article was written may have already changed by the time you read it.

These shifts directly affect whether an FTZ or bonded warehouse remains the right choice – and how each structure should be configured. The inverted tariff benefit in FTZs depends on rate differentials between components and finished products, and those differentials change when tariff rates are adjusted. Mandatory privileged foreign status requirements for goods subject to trade remedy tariffs limit certain FTZ advantages. And potential tariff reductions – whether through court decisions, legislative action, or negotiated trade agreements – could make bonded warehousing more attractive for goods where the withdrawal-time rate assessment works in the importer’s favor.

This is exactly the kind of monitoring that a proactive logistics and compliance partner should be doing on your behalf. Unicargo’s trade compliance team tracks Section 301 actions, Section 232 developments, antidumping and countervailing duty orders, Federal Register notices, and CBP guidance updates as a matter of course. When something changes that affects a client’s duty deferral strategy, the conversation happens before the impact hits – not in response to a surprise duty bill.

How Unicargo Helps Importers Navigate Duty Deferral and Trade Compliance

For most importers, the gap between understanding that an FTZ or bonded warehouse could save money and actually capturing those savings comes down to execution. The strategy is only as good as the operational infrastructure behind it – and that infrastructure spans freight, customs, warehousing, and compliance in ways that can’t be addressed by any single-function provider.

Unicargo is built around exactly this kind of integrated execution. Our model brings freight forwarding, customs brokerage, warehousing, and trade compliance advisory under one coordinated operating structure, which means that the handoffs between functions – where most problems originate – are internal processes rather than external dependencies.

Customs clearance. Our customs brokerage capabilities include automated classification, duty calculation, and entry filing. Whether you’re filing weekly entries in an FTZ or processing individual withdrawals from a bonded warehouse, our systems ensure accuracy and compliance at every step. Classification accuracy is monitored continuously – not just at the point of entry – so that changes in tariff schedules, product modifications, or new trade remedy orders are caught before they affect your duty position.

Trade compliance advisory. Tariff policy is a moving target. Our team monitors Section 301 actions, Section 232 developments, antidumping and countervailing duty orders, and new trade investigations. When changes affect your import strategy, we advise on adjustments – whether that means reclassifying goods, shifting between FTZ and bonded warehouse structures, or adapting entry procedures to capture new savings. This isn’t a reactive service triggered by client requests; it’s an ongoing posture built into how we manage every account.

International freight forwarding. Getting goods to the right facility starts with coordinated international shipping. Our freight operations span ocean, air, and ground freight from origin countries, with a team physically based in China managing origin-side coordination. That means documentation, ISF filings, in-bond procedures, and carrier bookings are managed as a unified workflow rather than assembled from separate moving parts. For complex supply chains that require the precision timing of FTZ or bonded warehouse intake, this integration is not a convenience – it’s a prerequisite for the strategy to work.

Warehousing across 13 global facilities. Our warehousing network supports both storage and fulfillment operations, with facilities positioned to serve FTZ and bonded warehouse workflows. For importers with distribution requirements – including those shipping to domestic fulfillment centers or international destinations – our warehousing capabilities connect directly to the duty deferral structure rather than operating downstream from it.

Supply chain visibility. Our digital platform gives you real-time visibility into shipment status, customs clearance progress, inventory levels, and duty exposure. You see exactly where your goods are and what your cost position looks like at every stage – which matters especially in a tariff environment where rate changes can affect the value of deferred duties and the timing of withdrawal decisions.

Dedicated logistics managers. Every client works with a dedicated logistics manager who coordinates across freight, customs, and warehousing. When issues arise – and in international logistics, they always do – you have a single point of contact who knows your account, understands your duty deferral structure, and can resolve problems quickly before they compound.

As an Amazon SPN partner with teams in the U.S., Israel, and China, Unicargo works with importers across the full spectrum – from established manufacturers evaluating FTZ subzone activation to mid-market distributors using bonded warehousing to manage cash flow around seasonal demand cycles. The common thread isn’t the size of the operation; it’s the combination of complexity and the need for an integrated partner who can manage it.

Conclusion

The FTZ vs bonded warehouse decision ultimately comes down to matching the right structure to your import profile. If you manufacture or assemble imported components, import at high volume, or need unlimited storage flexibility, an FTZ offers savings potential that bonded warehousing can’t match. If your needs are simpler, deferring duties on stored goods, holding inventory before committing to domestic entry, or managing re-exports without heavy compliance overhead, a bonded warehouse may be the more practical and cost-effective choice.

Neither option is universally better. The right answer depends on your duty exposure, product operations, re-export patterns, inventory cycles, and operational capacity. And in a trade environment where tariff policy can shift as quickly as a court ruling or a new Federal Register notice, this is an ongoing strategic decision – not a one-time choice.

What’s consistent across both options is the need for customs and logistics expertise. Correct classification, compliant entries, coordinated freight, and proactive trade compliance monitoring are what turn either structure from a theoretical benefit into real cost savings. That requires a partner who is embedded in your supply chain, not standing outside it.

Ready to find out which duty deferral strategy fits your business? Let Unicargo’s trade compliance and logistics team review your import data, duty exposure, and supply chain to determine whether an FTZ, bonded warehouse, or hybrid approach saves you the most.

FAQ

What is the difference between a Foreign Trade Zone and a bonded warehouse?

Both defer customs duties until goods enter U.S. domestic commerce, and both eliminate duties on goods that are re-exported. The key differences: FTZs allow manufacturing, assembly, and processing of goods, while bonded warehouses are limited to storage and minor manipulation (cleaning, sorting, repacking). FTZs offer the inverted tariff benefit, allowing manufacturers to pay the lower finished-product duty rate. FTZs support weekly entry consolidation that reduces merchandise processing fees. And bonded warehouses impose a five-year storage limit, while FTZs have no time restriction. FTZs carry higher compliance requirements and costs, making them better suited for high-volume importers and manufacturers, while bonded warehouses offer a simpler path for businesses focused on storage and distribution.

What is the duty deferral benefit for FTZ?

FTZ duty deferral means customs duties are not assessed until goods leave the zone and formally enter U.S. commerce. If goods are re-exported, destroyed, or scrapped within the zone, duties are eliminated entirely. Beyond deferral, FTZs offer duty reduction through the inverted tariff benefit (paying the lower finished-product rate when applicable) and weekly entry consolidation that reduces merchandise processing fees. There is no time limit on how long goods can remain in an FTZ, making deferral effectively indefinite for goods that aren’t withdrawn for domestic consumption.

What are the disadvantages of a Foreign Trade Zone?

FTZs involve higher setup and ongoing compliance costs compared to bonded warehouses, including FTZ Board activation, operator fees, and investment in compliant inventory systems. Recordkeeping and reporting requirements are more complex, with oversight from both the FTZ Board and CBP. Production activity requires specific FTZ Board authorization, which adds time and administrative burden. Recent trade policy changes have required mandatory privileged foreign status for goods subject to Section 301 and other trade remedy tariffs, limiting the inverted tariff benefit for those products. For low-volume importers or businesses with simple storage needs, the costs may outweigh the benefits.

Can a facility operate as both an FTZ and a bonded warehouse?

Not simultaneously in the same physical space – the two structures operate under different regulatory frameworks (FTZ Board + CBP versus CBP alone) with different legal designations. However, a company can absolutely use both structures for different product lines or import flows. Some logistics facilities are located near both FTZ sites and bonded warehouses, enabling hybrid strategies where manufacturing inputs go through the FTZ and distribution inventory is held in bonded storage. A logistics partner experienced with both structures can help coordinate these parallel workflows efficiently.

How do I know if my import volume justifies an FTZ or bonded warehouse?

Start with your annual duty expenditure, import frequency, re-export percentage, and average inventory holding period. For bonded warehousing, the threshold is relatively low – if your duty deferral and re-export savings exceed the cost of bonding and bonded storage fees, it’s worth pursuing. For FTZs, the threshold is higher because of greater setup and operating costs. Generally, importers with annual duty exposure in the six-figure range, frequent entries (where weekly consolidation adds up), or meaningful manufacturing activity should evaluate FTZ participation. The most reliable way to determine fit is to have a customs and logistics partner analyze your actual import data against the cost structure of each option.

Are FTZ benefits still valuable with changing tariff policies?

FTZ benefits can actually become more valuable during periods of tariff escalation – higher duty rates mean more cash flow at stake and greater savings from deferral and elimination on re-exports. However, changing rates require ongoing monitoring and potential reclassification. The mandatory privileged foreign status requirement for goods under trade remedy tariffs limits certain FTZ advantages, particularly the inverted tariff benefit. And if tariffs are expected to decrease – whether through legal rulings, trade negotiations, or legislative change – bonded warehousing (which applies the rate at time of withdrawal) may offer a strategic advantage over FTZ privileged foreign status (which locks in the rate at admission). The bottom line: FTZ benefits remain substantial, but maximizing them in a volatile tariff environment requires a compliance partner who tracks policy changes proactively and adjusts your strategy accordingly. Always verify current tariff rates, applicable statutes, and HS code classifications with your customs broker or trade counsel before making structural decisions, as this area changes frequently.

Need help with your next warehousing or shipping arrangements?

Contact us here, and we’ll get our team of experts to review your needs and offer you several alternatives to what you’re currently running.